Welcome to Grupo Spurrier

Grupo Spurrier is the leading company in the provision of strategic information on economic and political issues regarding Ecuador, which we monitor through Weekly Analysis and Análisis Semanal. We specialize in economic research, competition advice, market research, business plans, and workshops in economic scenarios and regulatory changes.

Weekly Analysis Briefs

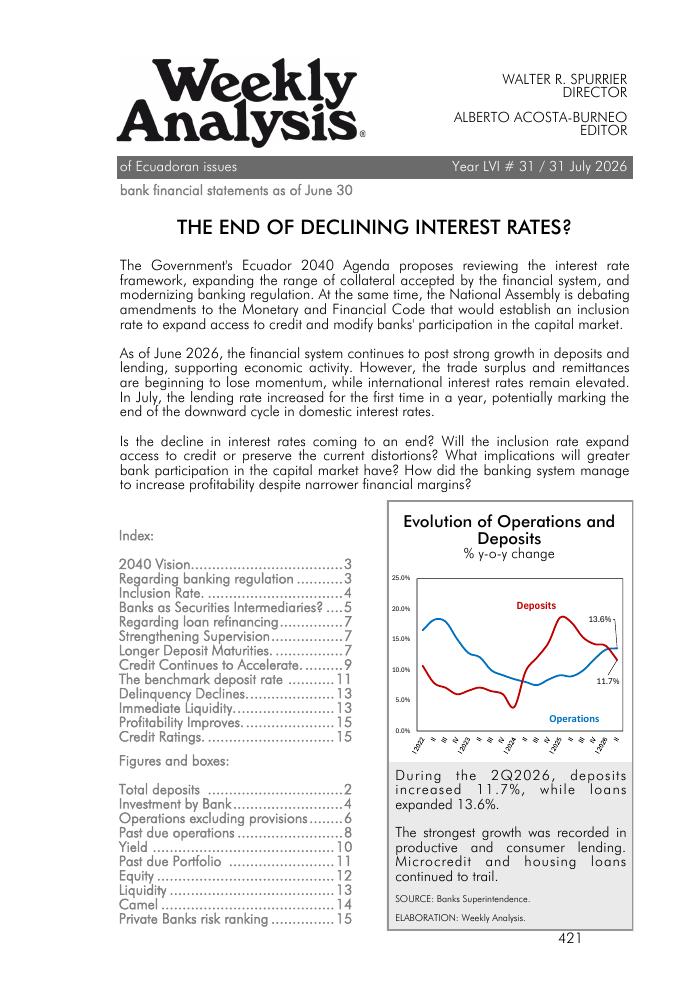

WA-2026-31: THE END OF DECLINING INTEREST RATES?

The Government's Ecuador 2040 Agenda proposes reviewing the interest rate framework, expanding the range of collateral accepted by the financial system, and modernizing banking regulation. At the same time, the National Assembly is debating amendments to the Monetary and Financial Code that would establish an inclusion rate to expand access to credit and modify banks' participation in the capital market. As of June 2026, the financial system continues to post strong growth in deposits and lending, supporting economic activity. However, the trade surplus and remittances are beginning to lose momentum, while international interest rates remain elevated. In July, the lending rate increased for the first time in a year, potentially marking the end of the downward cycle in domestic interest rates. Is the decline in interest rates coming to an end? Will the inclusion rate expand access to credit or preserve the current distortions? What implications will greater bank participation in the capital market have? How did the banking system manage to increase profitability despite narrower financial margins?

WA-2026-30: SOLUTIONS REMAIN ELUSIVE

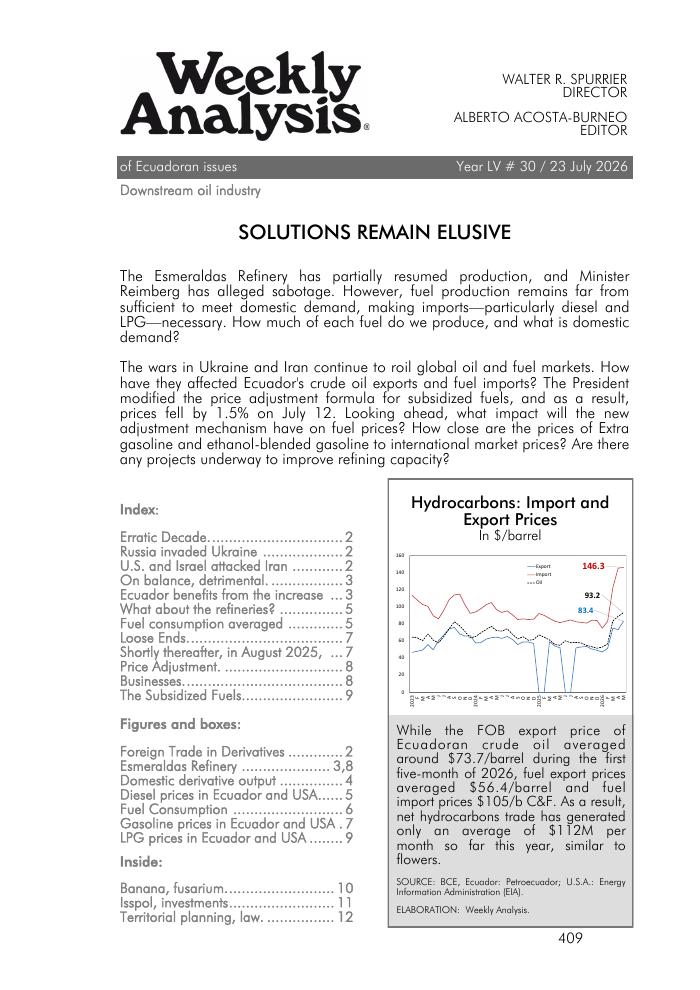

The Esmeraldas Refinery has partially resumed production, and Minister Reimberg has alleged sabotage. However, fuel production remains far from sufficient to meet domestic demand, making imports—particularly diesel and LPG—necessary. How much of each fuel do we produce, and what is domestic demand? The wars in Ukraine and Iran continue to roil global oil and fuel markets. How have they affected Ecuador's crude oil exports and fuel imports? The President modified the price adjustment formula for subsidized fuels, and as a result, prices fell by 1.5% on July 12. Looking ahead, what impact will the new adjustment mechanism have on fuel prices? How close are the prices of Extra gasoline and ethanol-blended gasoline to international market prices? Are there any projects underway to improve refining capacity?

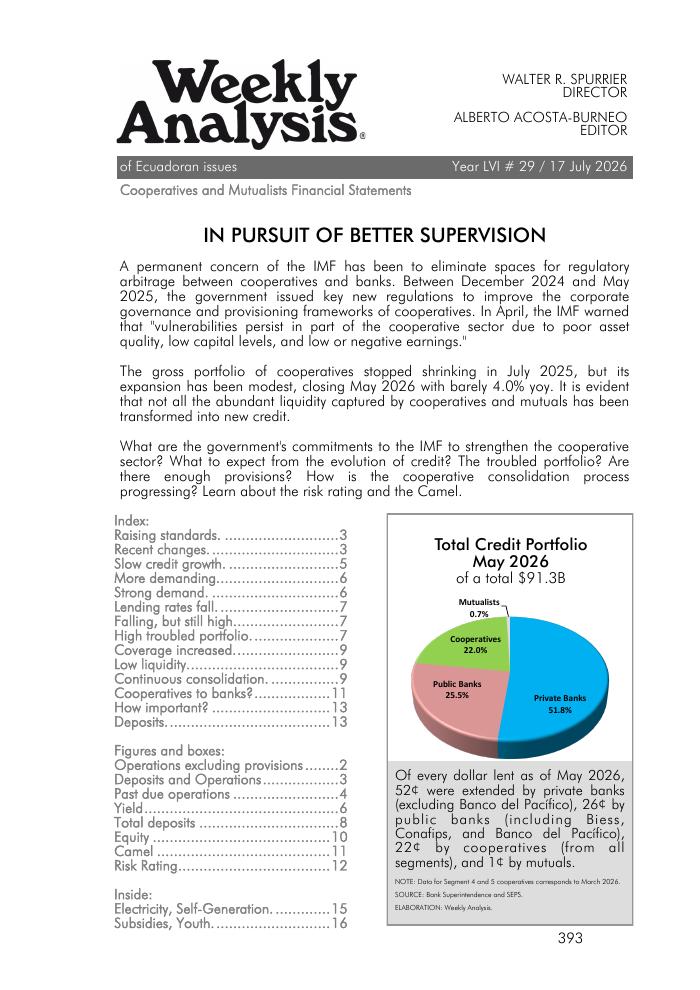

WA-2026-29: IN PURSUIT OF BETTER SUPERVISION

A permanent concern of the IMF has been to eliminate spaces for regulatory arbitrage between cooperatives and banks. Between December 2024 and May 2025, the government issued key new regulations to improve the corporate governance and provisioning frameworks of cooperatives. In April, the IMF warned that "vulnerabilities persist in part of the cooperative sector due to poor asset quality, low capital levels, and low or negative earnings." The gross portfolio of cooperatives stopped shrinking in July 2025, but its expansion has been modest, closing May 2026 with barely 4.0% yoy. It is evident that not all the abundant liquidity captured by cooperatives and mutuals has been transformed into new credit. What are the government's commitments to the IMF to strengthen the cooperative sector? What to expect from the evolution of credit? The troubled portfolio? Are there enough provisions? How is the cooperative consolidation process progressing? Learn about the risk rating and the Camel.

WA-2026-28: CONSTRUCTION LEADS GROWTH

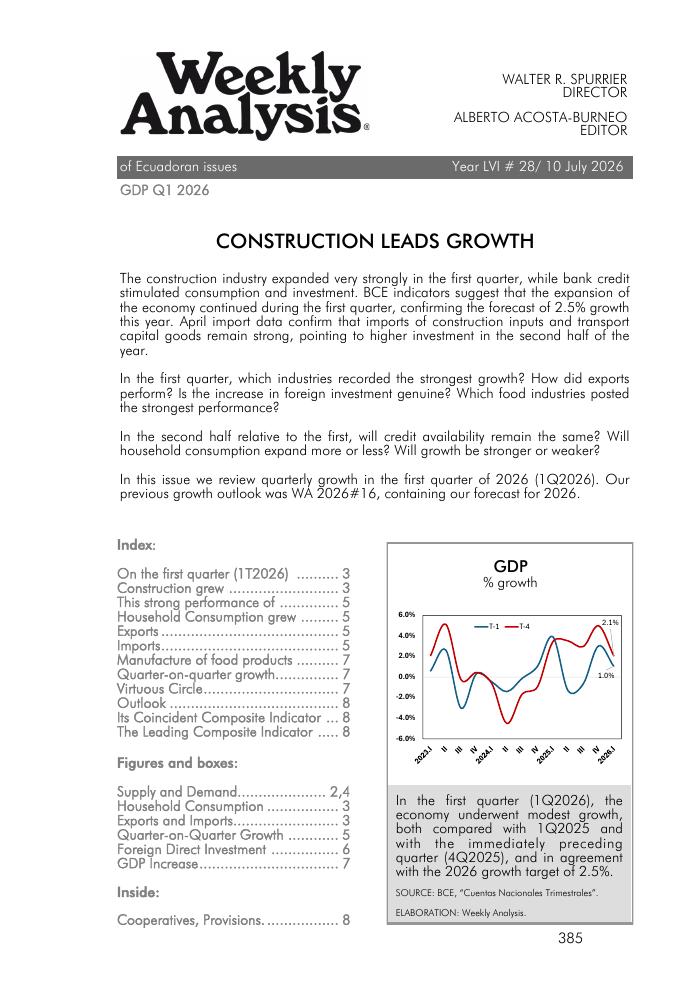

The construction industry expanded very strongly in the first quarter, while bank credit stimulated consumption and investment. BCE indicators suggest that the expansion of the economy continued during the first quarter, confirming the forecast of 2.5% growth this year. April import data confirm that imports of construction inputs and transport capital goods remain strong, pointing to higher investment in the second half of the year. In the first quarter, which industries recorded the strongest growth? How did exports perform? Is the increase in foreign investment genuine? Which food industries posted the strongest performance? In the second half relative to the first, will credit availability remain the same? Will household consumption expand more or less? Will growth be stronger or weaker? In this issue we review quarterly growth in the first quarter of 2026 (1Q2026). Our previous growth outlook was WA 2026#16, containing our forecast for 2026.

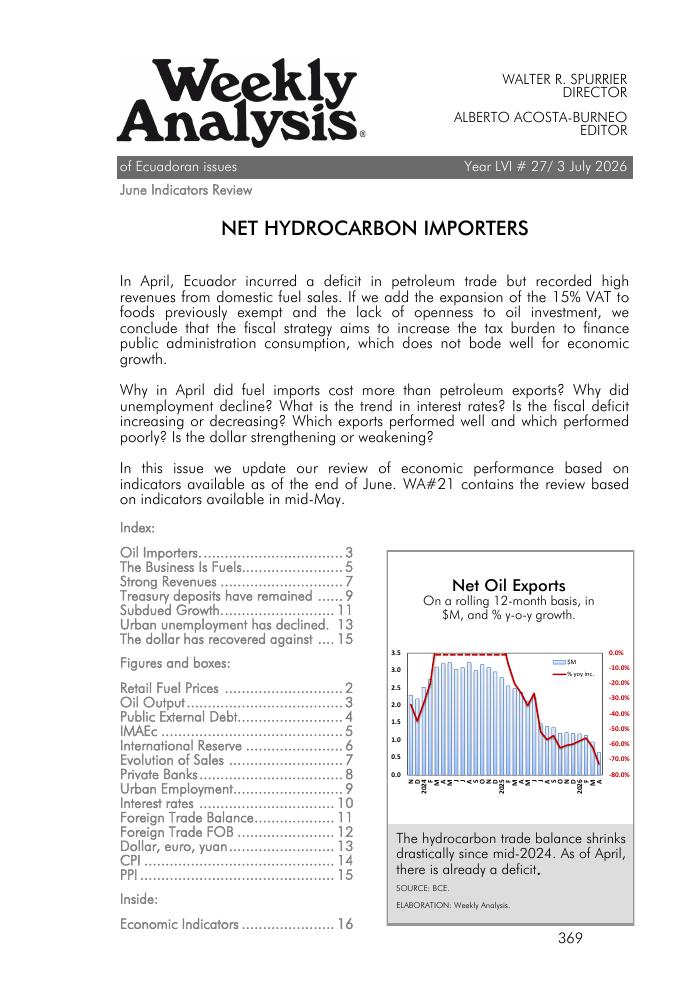

WA-2026-27: NET HYDROCARBON IMPORTERS

In April, Ecuador incurred a deficit in petroleum trade but recorded high revenues from domestic fuel sales. If we add the expansion of the 15% VAT to foods previously exempt and the lack of openness to oil investment, we conclude that the fiscal strategy aims to increase the tax burden to finance public administration consumption, which does not bode well for economic growth. Why in April did fuel imports cost more than petroleum exports? Why did unemployment decline? What is the trend in interest rates? Is the fiscal deficit increasing or decreasing? Which exports performed well and which performed poorly? Is the dollar strengthening or weakening? In this issue we update our review of economic performance based on indicators available as of the end of June. WA#21 contains the review based on indicators available in mid-May.

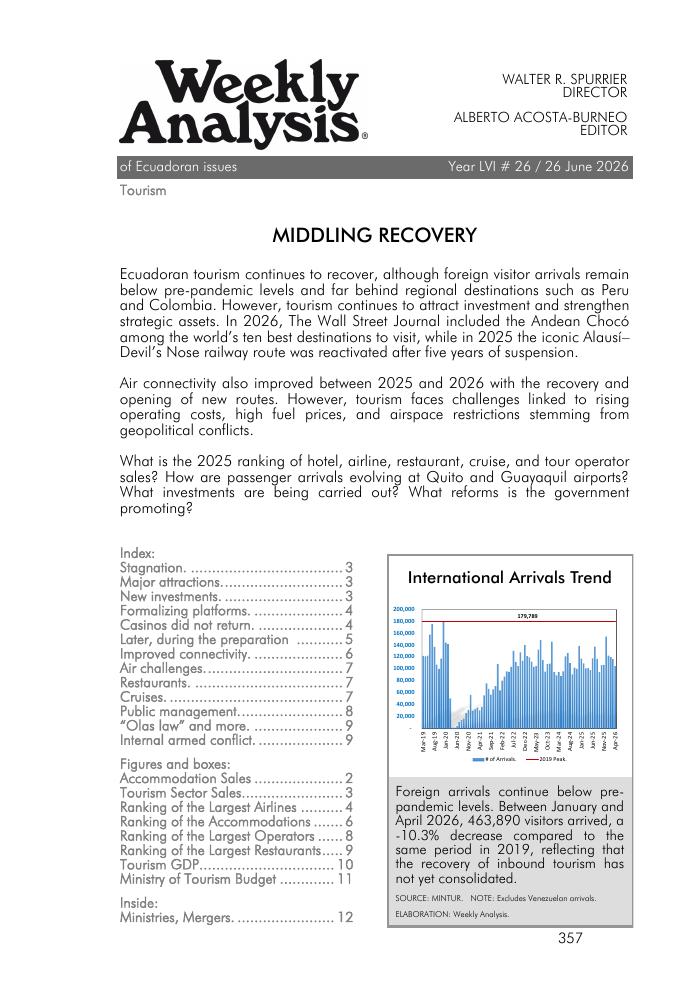

WA-2026-26: MIDDLING RECOVERY

Ecuadoran tourism continues to recover, although foreign visitor arrivals remain below pre-pandemic levels and far behind regional destinations such as Peru and Colombia. However, tourism continues to attract investment and strengthen strategic assets. In 2026, The Wall Street Journal included the Andean Chocó among the world’s ten best destinations to visit, while in 2025 the iconic Alausí–Devil’s Nose railway route was reactivated after five years of suspension. Air connectivity also improved between 2025 and 2026 with the recovery and opening of new routes. However, tourism faces challenges linked to rising operating costs, high fuel prices, and airspace restrictions stemming from geopolitical conflicts. What is the 2025 ranking of hotel, airline, restaurant, cruise, and tour operator sales? How are passenger arrivals evolving at Quito and Guayaquil airports? What investments are being carried out? What reforms is the government promoting?